Data for me but not for thee: two roadblocks on the path to financial transparency

Offshore wealth is a lot more visible than it used to be. While in the early 2010s, most governments struggled to know how much their citizens stashed abroad, the picture changed with the introduction of a new automatic exchange-of-information agreement penned by the OECD. Countries that signed up to the Common Reporting Standard (CRS) were required to regularly exchange information with each other on the financial wealth their respective taxpayers held offshore. Now, more than 120 countries regularly exchange this information, covering more than €13 trillion in assets. Recent work by those of us at the International Tax Observatory has shown that while these agreements don’t yet fully capture everything held offshore, they have vastly improved what tax authorities can detect.

Research shows that the information that tax authorities receive via automatic exchange-of-information agreements can be powerful too. Tax authorities that use this information well stand not only to discourage the use of tax havens for tax evasion, but also to encourage former evaders to repatriate their wealth back home, where its proceeds can be taxed. The CRS does have some structural flaws, and many tax authorities are still learning how to use CRS data to better target their auditing and other enforcement efforts. Despite this, the OECD already reports that, in aggregate, better transparency has led to the recouping of over a hundred billion dollars worth of tax revenue.

The question is whether the benefit of these information exchange regimes can also be enjoyed by countries in the Global South. Households in low-and lower-middle income countries hold a higher share of their financial wealth offshore than those in other country groups. Given that countries in the global south already struggle to raise much revenue from personal income tax regimes, access to automatic exchange-of-information data could help move the needle. However, an analysis in a new research note published by the ITO this week shows that two of the regions in the Global South that could benefit the most, sub-Saharan African and Latin America and the Caribbean, both struggle to access the information they need.

The African participation problem

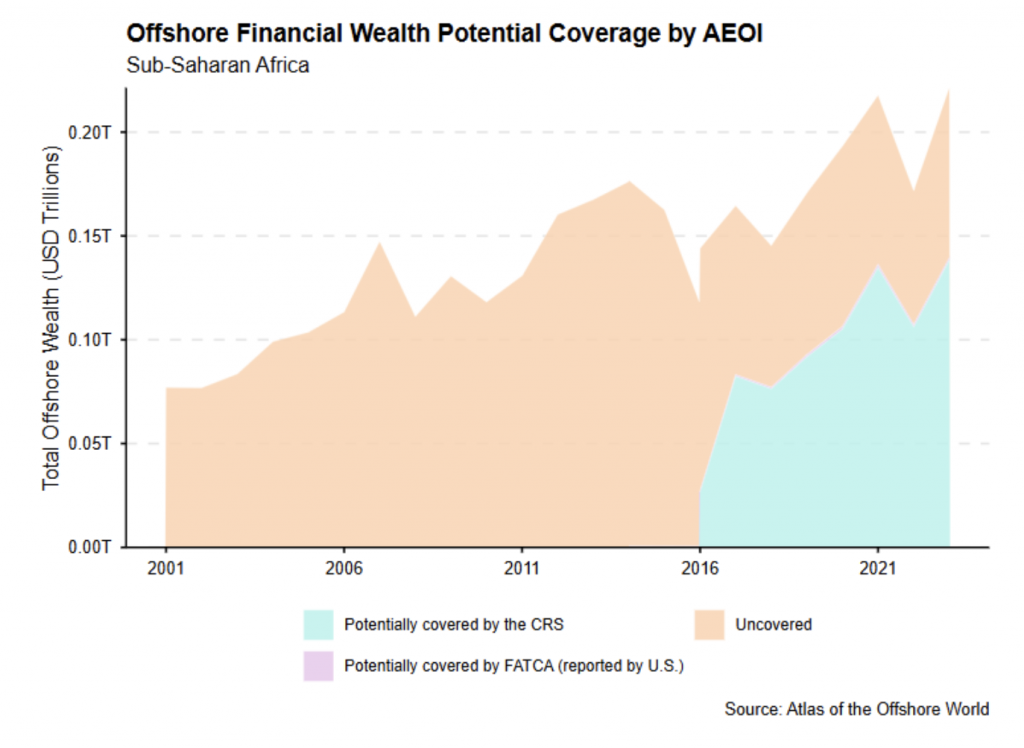

Sub-Saharan African households hold most of their offshore wealth in European tax havens, all of whom have long since adopted the CRS. Despite this, most African countries don’t participate themselves: in a recent conference that we hosted on progress on financial transparency, Dr Ezera Madzivanyika from the African Tax Administration Forum lamented the fact that only a handful of countries in Sub-Saharan Africa have joined the CRS. By our estimates, only a little more than half of offshore wealth owned by households from the region is currently covered, largely due to the participation of large countries like Nigeria, South Africa and Kenya.

Why is the rest of the continent hesitant to participate? The answer lies in part in the way the CRS was designed: in order to benefit from it, you need to share data yourself. Implementing the policies and frameworks to require all of your domestic financial institutions to carefully collect their foreign customers’ data and then store and transmit it in a secure manner is a challenging task even for richer, high-capacity countries. Many lower-income countries in the region would struggle to do so, and so lose out on the ability to receive such information on their own taxpayers.

One answer to this problem is one that many multilateral institutions have already embraced: provide African countries with the technical support they need to meet the OECD’s exacting standards for implementing the CRS. But there is another possibility: the OECD could tweak the rules to allow low-capacity countries (particularly those which are demonstrably not offshore financial centers) to begin receiving information before they have fully implemented the ability to share it themselves.

Latin America’s America problem

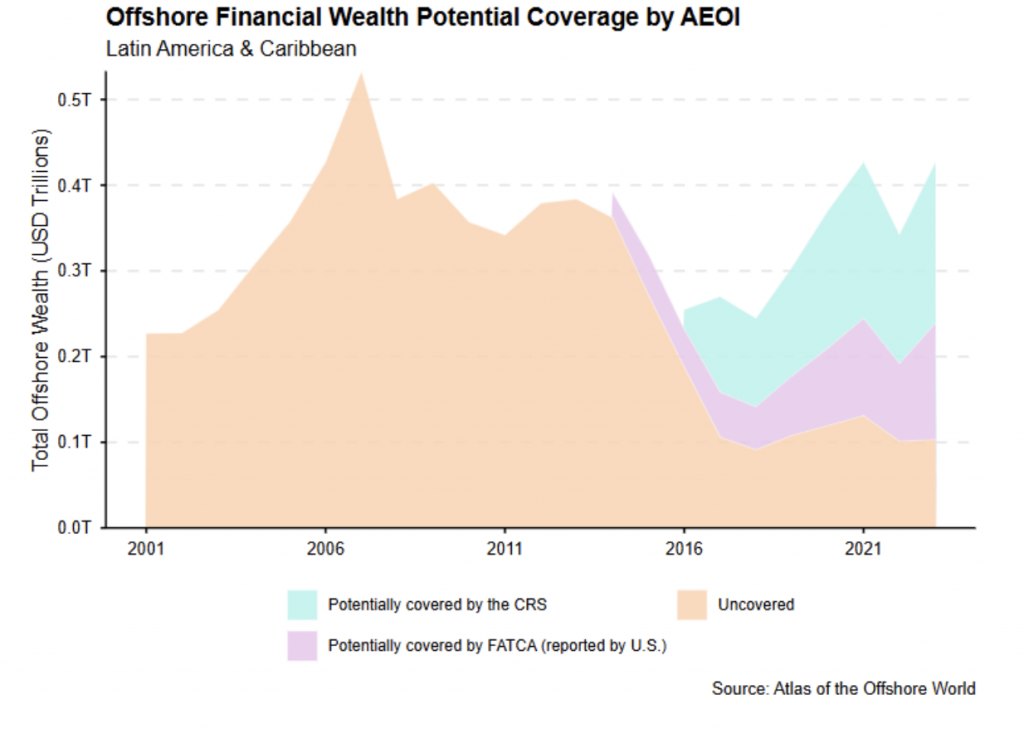

In the latest data published on our data portal, the Atlas of the Offshore World, we show that a large share of households in Latin America prefer to keep their financial assets in American financial centers, with the United States being a major hub.* This presents a challenge: the US does not participate in the CRS, so tax authorities in the region are unable to rely on it for understanding what their taxpayers hold there.

In theory, the US’s own information sharing agreement, the Foreign Account Tax Compliance Act (FATCA), should act as a backstop. FATCA mandates foreign banks to send automatic information on US taxpayers back to the IRS every year. However, many countries have signed intergovernmental agreements with the US, which typically include a reciprocity provision, requiring the IRS to remit some information back to the latter. It is arguably due to this putative reciprocity that the US has received a pass from the OECD on its lack of participation in the CRS. But because the IRS does not require American banks to look through companies, particularly small shell companies, to understand who ultimately owns them, it is very easy to hold financial wealth in the US with little chance of being discovered.

How much is left on the table? By our most recent estimates, about 44% of all Latin American offshore financial wealth sits in the US, the majority of which is unlikely to be picked up by FATCA. Until the US decides to either join the Common Reporting Standard or force its financial sector to do more detective work, tax authorities in the Latin America and Caribbean region will struggle to uncover what their citizens hold there.

* This data is taken from a recent ITO Publication.

by Matthew Collin, Sarah Godar, Juan Vergara, Giulia Varaschin